Fact-checked by the The Insurance Scout editorial team

Quick Answer

To dispute an insurance settlement, you must document your damages thoroughly, submit a formal written appeal to your insurer, and escalate to your state insurance commissioner if the response is unsatisfactory. As of July 2026, policyholders who hire a public adjuster recover an average of 747% more than the initial offer. Most disputes are resolved within 30–90 days when handled correctly.

If your insurance company offered you far less than your claim is worth, you can dispute an insurance settlement — and in 2026, more policyholders are winning those disputes than ever before. According to the Insurance Information Institute, insurers underpay or deny millions of legitimate claims every year, leaving billions of dollars on the table that policyholders are legally entitled to. The process is not automatic, but with the right documentation and escalation strategy, you have real leverage.

The urgency is higher in 2026 than it has been in years. A combination of record catastrophic weather events, inflation-driven repair costs, and tightening insurer profit margins has pushed more carriers to issue low initial settlements as a matter of standard practice. Consumer advocacy organizations report that complaint volumes filed with state insurance departments rose by 23% between 2023 and 2025, signaling that policyholders are no longer accepting lowball offers without a fight.

This guide is for anyone who received a settlement offer that does not cover actual repair costs, lost income, or medical bills — whether from a homeowners, auto, or health insurance claim. By the end, you will know exactly how to build a dispute case, who to call, and when to escalate to legal action.

Key Takeaways

- Policyholders who formally dispute an insurance settlement recover an average of $1,500–$10,000 more per claim, according to data from the California Department of Insurance.

- Public adjusters negotiate on your behalf and typically secure settlements 747% higher than initial offers, per the National Association of Public Insurance Adjusters (NAPIA).

- Every U.S. state has an insurance commissioner’s office where you can file a complaint for free — most states require insurers to respond within 15–45 business days.

- Appraisal clauses, written into most standard homeowners policies, give you the legal right to an independent damage assessment without going to court, per the National Association of Insurance Commissioners (NAIC).

- Bad faith insurance lawsuits can result in settlements that exceed the original claim amount by 2–3 times, including attorney fees and punitive damages in some states.

- Filing a state department complaint resolves roughly 40% of insurance disputes without any legal action, according to the NAIC Consumer Complaint Database.

In This Guide

- Step 1: How Do You Know If Your Insurance Settlement Is Too Low?

- Step 2: What Evidence Do You Need to Dispute an Insurance Settlement?

- Step 3: How Do You File a Formal Appeal With Your Insurance Company?

- Step 4: Should You Hire a Public Adjuster or an Insurance Attorney?

- Step 5: How Do You File a Complaint With Your State Insurance Commissioner?

- Step 6: How Does the Appraisal Process Work for Insurance Disputes?

- Step 7: When Should You Sue Your Insurance Company for a Bad Faith Settlement?

- Frequently Asked Questions

Step 1: How Do You Know If Your Insurance Settlement Is Too Low?

Your settlement is likely too low if the offer does not cover the documented cost of repairs, replacement, or losses as defined by your actual policy terms. The first step is to read your policy — specifically the declarations page, coverage limits, and any actual cash value (ACV) versus replacement cost value (RCV) language — before concluding the insurer made an error.

How to Do This

Pull your policy documents and compare the insurer’s itemized settlement breakdown against your own damage estimates. Pay close attention to whether your policy pays ACV (depreciated value) or RCV (full replacement cost). This distinction alone can account for thousands of dollars in gap. Our detailed breakdown on actual cash value vs replacement cost coverage explains exactly how insurers calculate each and what you are actually owed.

Request a complete copy of the adjuster’s inspection report and the insurer’s damage estimate worksheet. You are legally entitled to these documents in every U.S. state. Look for missing line items, underestimated labor costs, or damage categories your adjuster overlooked entirely.

What to Watch Out For

Many insurers issue low ACV payments quickly and count on policyholders not knowing they can supplement the claim once contractors assess the full damage. Do not sign a final release or accept payment marked “payment in full” before you are certain all damage is accounted for. Cashing a check without checking this language can legally settle your claim.

According to the NAIC, the top reason for homeowner insurance complaints in 2024 was unsatisfactory settlement offers — accounting for more than 34% of all property insurance complaints filed nationally.

Step 2: What Evidence Do You Need to Dispute an Insurance Settlement?

To successfully dispute an insurance settlement, you need independent repair estimates, photographs, expert assessments, and receipts — all organized in a written file you can present to your insurer or a third party. The stronger your documentation, the less leverage the insurer has to defend a low offer.

How to Do This

Start by getting at least two or three independent contractor estimates for the full scope of repairs. Use licensed, local contractors familiar with current material and labor costs in your area — costs have risen significantly due to inflation, and 2020 or 2021 pricing tables still used by some adjusters are outdated. For auto claims, get a written estimate from a certified auto body shop rather than relying solely on the insurer’s preferred vendor.

Compile the following into a single organized claim package:

- Timestamped photographs and video of all damage

- Pre-loss documentation (receipts, appraisals, photos showing prior condition)

- Two to three independent repair or replacement estimates

- A written summary of how the damage occurred

- Medical records and bills, if the claim involves bodily injury

- A copy of your insurance policy with relevant sections highlighted

- All correspondence with your insurer, including dates and contact names

What to Watch Out For

Avoid submitting a dispute without independent estimates — your personal opinion of value is not sufficient evidence. If you previously made common errors on your original claim, review the guide on homeowners insurance mistakes that lead to denied claims to ensure your dispute does not repeat those problems.

Use a numbered, tabbed binder or a clearly organized PDF when submitting your dispute package. Claims departments process dozens of files daily — a well-organized submission gets reviewed more thoroughly and stands out as a serious challenge to the initial offer.

Step 3: How Do You File a Formal Appeal With Your Insurance Company?

Filing a formal written appeal is the first official step to dispute an insurance settlement, and it must be done in writing — not by phone — to create a documented paper trail. Most insurers have an internal appeals process, and triggering it officially starts the clock on response deadlines they are required to meet under state law.

How to Do This

Write a formal dispute letter addressed to your insurer’s claims department. Send it via certified mail with return receipt requested so you have proof of delivery. Your letter should include:

- Your policy number and claim number

- A clear statement that you are disputing the settlement amount

- A specific dollar amount you are requesting and why

- A list of attached supporting documents (estimates, photos, reports)

- A request for a written response within a defined timeframe (14–30 days is reasonable)

Most state insurance codes require insurers to acknowledge disputes within 10 business days and provide a substantive written response within 30–45 days. Check your state’s specific deadlines on your state insurance department’s website.

What to Watch Out For

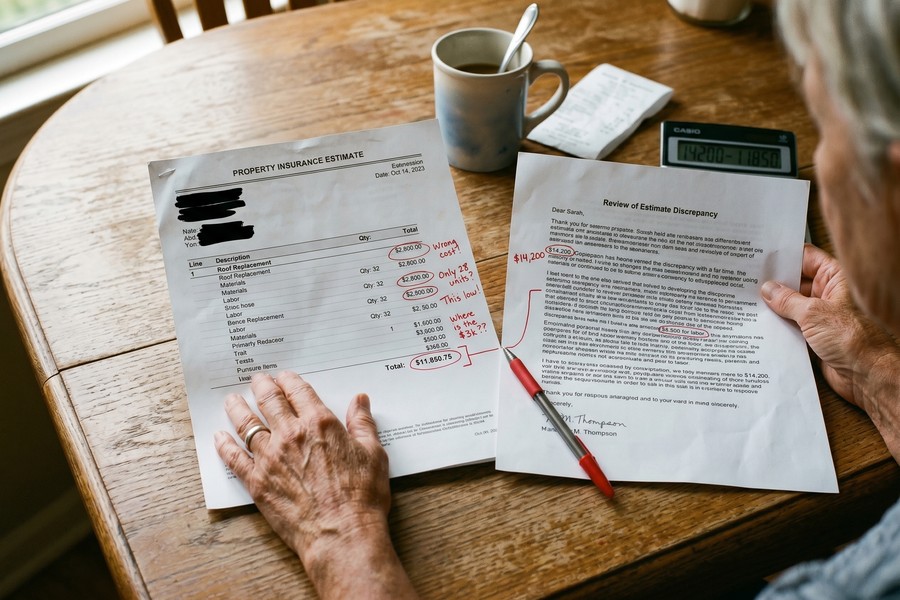

Be specific about the dollar gap, not just your frustration. A letter that says “I think this is too low” is weaker than one that says “Your estimate of $8,400 does not account for the $14,200 in documented damage per the attached contractor reports.” Specificity makes your case far harder to dismiss.

Never accept a verbal assurance over the phone that “we’ll look into it.” Verbal promises are not binding. Every communication about your dispute must be in writing. Follow up any phone call with an email summarizing what was discussed and asking for written confirmation.

Here is a comparison of the main approaches policyholders use to dispute insurance settlements, with real-world numbers to help you choose the right path:

| Dispute Method | Average Time to Resolution | Average Payout Increase | Cost to Policyholder |

|---|---|---|---|

| Internal Appeal (DIY) | 14–45 days | 10–30% above initial offer | $0 |

| Public Adjuster | 30–90 days | Up to 747% above initial offer | 5–15% of final settlement |

| State Department Complaint | 30–60 days | 15–40% above initial offer | $0 |

| Appraisal / Mediation | 60–120 days | 20–60% above initial offer | $200–$1,500 (shared appraiser cost) |

| Insurance Attorney / Bad Faith Lawsuit | 6–24 months | 100–300% above initial offer | 30–40% contingency fee |

Step 4: Should You Hire a Public Adjuster or an Insurance Attorney?

You should hire a public adjuster when your claim involves complex property damage and you want a professional negotiator without going to court. You should hire an insurance attorney when your insurer is acting in bad faith, delaying unreasonably, or outright denying a valid claim. Both options are most effective when the settlement gap exceeds $5,000.

How to Do This

A public adjuster is a licensed claims professional who works exclusively for policyholders — not the insurance company. They assess your damage independently, document it professionally, and negotiate directly with your insurer. Find a licensed public adjuster through the NAPIA Find-a-Public-Adjuster directory. Most work on contingency, taking 5–15% of the final settlement, so there is no upfront cost.

An insurance bad faith attorney is appropriate when your insurer denies your claim without a legitimate reason, fails to investigate in a timely manner, or makes a settlement offer so unreasonably low it constitutes bad faith under your state’s insurance code. Many insurance attorneys work on contingency as well, meaning you pay nothing unless you win.

“Policyholders who engage a licensed public adjuster early in the dispute process almost always see a materially better outcome. The insurer’s adjuster works for the company — having your own advocate levels the playing field significantly.”

What to Watch Out For

Not all “claims advocates” are licensed public adjusters. Verify licensure through your state insurance department before signing any agreement. Also confirm the adjuster’s fee is capped — some states limit public adjuster fees to 10% for non-catastrophe claims and 20% for disaster declarations.

A Florida Office of Insurance Regulation study found that policyholders using public adjusters received an average settlement of $22,266 compared to $18,659 for those who did not — and in catastrophe-declared areas, the gap was far larger, with represented claims averaging 574% more than unrepresented claims.

Step 5: How Do You File a Complaint With Your State Insurance Commissioner?

Filing a complaint with your state insurance commissioner is free, requires no attorney, and puts formal regulatory pressure on your insurer to respond. Every state has an insurance department that oversees carrier conduct, and a formal complaint triggers a mandatory investigation that insurers take seriously.

How to Do This

Visit your state insurance department’s website and locate the consumer complaint section. Most states offer an online complaint portal. The NAIC Consumer Information Source provides links to every state’s insurance department. Submit your complaint along with copies of all correspondence, your policy, the settlement offer, and your independent estimates.

After filing, your insurer is legally required to respond to the state department — usually within 15–45 business days depending on the state. The commissioner’s office will send you the insurer’s response and may mediate a resolution. Insurers who frequently receive complaints face increased regulatory scrutiny, higher compliance costs, and potential license action — strong incentive to resolve your dispute.

What to Watch Out For

A state complaint is not a court proceeding — the commissioner cannot force an insurer to pay a specific dollar amount in most states. What it can do is establish a documented record of the insurer’s conduct, which becomes valuable evidence if you later pursue legal action. Think of it as a powerful escalation tool, not a final resolution mechanism.

Mention your intent to file a state department complaint in your formal appeal letter before actually filing it. Many claims managers have authority to increase settlements without supervisor approval when regulatory action appears imminent — and your letter signals you know the process.

Step 6: How Does the Appraisal Process Work for Insurance Disputes?

The appraisal process is a binding, out-of-court dispute resolution mechanism built into most standard homeowners and auto insurance policies. You do not need to sue to trigger it — you simply invoke the appraisal clause in writing, and both sides hire independent appraisers who work toward a binding resolution.

How to Do This

Check your policy for the appraisal clause — it is typically found in the “Conditions” or “Loss Settlement” section. To invoke it, send your insurer a written demand for appraisal via certified mail. Each side then selects a competent, impartial appraiser. If the two appraisers disagree, they jointly select an umpire whose decision is binding on both parties.

The cost of the umpire is typically shared equally. Your appraiser’s cost is your responsibility, but it is usually far less expensive than litigation. Appraisal is particularly effective for property damage disputes where the question is the dollar amount of loss — not whether coverage applies.

Some states also offer free or low-cost insurance mediation programs. Florida, for example, operates a state-sponsored mediation program through its Department of Financial Services that has resolved thousands of hurricane and property damage disputes without court involvement.

What to Watch Out For

Appraisal resolves the amount of loss — it does not resolve coverage disputes. If your insurer is denying the claim outright on coverage grounds, appraisal is not the right tool. In that case, you will need to pursue mediation, a state complaint, or legal action. Understanding your policy type also matters here — if you are unsure whether your coverage is named perils or open perils, reviewing the differences in named perils vs open perils coverage can clarify what your insurer is and is not required to pay.

Step 7: When Should You Sue Your Insurance Company for a Bad Faith Settlement?

You should pursue legal action when your insurer denies, underpays, or unreasonably delays a valid claim without legitimate justification — conduct that qualifies as insurance bad faith under state law. Lawsuits are the most powerful tool available to policyholders, but also the most time-intensive, typically taking 6–24 months to resolve.

How to Do This

Consult an insurance bad faith attorney. Most offer free initial consultations and work on a contingency fee basis — typically 30–40% of the recovery — so you pay nothing unless you win. Look for attorneys who specialize in first-party insurance claims in your state, as bad faith laws vary significantly by jurisdiction.

Bad faith conduct includes the following insurer actions:

- Failing to investigate your claim within a reasonable time

- Offering a settlement that has no reasonable relationship to the actual damages

- Misrepresenting policy terms to avoid paying a claim

- Denying a claim without providing a written explanation

- Withholding payment after liability has been established

In states with strong bad faith statutes — including California, Florida, and Texas — successful lawsuits can result in the original claim amount plus attorney fees, interest, and in egregious cases, punitive damages.

“Insurance companies are not charities — they have financial incentives to pay as little as possible. But the law exists precisely to protect policyholders from that pressure. Bad faith claims are one of the most underutilized legal remedies available to consumers.”

What to Watch Out For

Statutes of limitations on insurance lawsuits range from one to six years depending on the state and claim type. Do not delay consulting an attorney while waiting for the insurer to “come around.” The clock starts from the date of loss or denial, not from when you decide to act.

If your claim also involves a coverage decision affecting your overall financial safety net, it is worth reviewing how your broader insurance portfolio is structured — including whether you have umbrella insurance vs excess liability coverage in place to handle gap scenarios.

Be cautious of “demand letter mills” that send generic legal-sounding letters to insurers for a flat fee. These services rarely produce results and can signal to your insurer that you are not working with a legitimate attorney. Always consult a licensed insurance attorney before sending legal correspondence.

Frequently Asked Questions

How long do I have to dispute an insurance settlement after receiving an offer?

The time limit to dispute an insurance settlement depends on your state and policy type, but most states allow between one and five years from the date of loss to file a formal legal challenge. However, you should begin your dispute within 30–60 days of receiving a low offer to preserve evidence and meet internal insurer deadlines. Check your specific policy for any written dispute notice requirements, as some policies impose shorter windows for triggering appraisal clauses.

Can I dispute a car insurance settlement the same way I dispute a homeowners claim?

Yes — the core steps to dispute an insurance settlement apply to auto claims as well, though the tools differ slightly. For auto claims, you can request a second appraisal from an independent shop, invoke your policy’s appraisal clause if available, or file a complaint with your state insurance commissioner. Avoid the common errors outlined in this guide on auto insurance claim mistakes, as they can weaken your dispute before it begins.

What happens if I cash the insurance check — can I still dispute the settlement?

Cashing a check does not automatically end your ability to dispute if the check was not explicitly labeled as a “final payment” or “payment in full.” If you signed a release or the check clearly states it is final settlement, you may have waived further claims. Always read the check and any accompanying documents carefully before depositing, and consult an attorney if you are unsure what you signed.

How much does it cost to hire a public adjuster to fight an insurance settlement?

Public adjusters typically charge 5–15% of the final settlement amount, with no upfront fee. For catastrophe-declared events, some states cap fees at 20%. Because they only get paid if your settlement increases, they have strong incentive to maximize your recovery. Always verify the adjuster’s license and confirm the fee structure in writing before signing an engagement agreement.

What is insurance bad faith and how do I know if my insurer is doing it?

Insurance bad faith occurs when an insurer unreasonably denies, delays, or underpays a valid claim without a legitimate basis. Common signs include receiving a denial with no written explanation, an offer that is dramatically below documented damages, or repeated delays in adjuster contact. If you believe your insurer is acting in bad faith, consult an insurance attorney immediately — most states impose penalties on insurers who engage in this conduct, including attorney fee shifting and punitive damages.

Should I get a lawyer before filing a complaint with the insurance department?

You do not need an attorney to file a complaint with your state insurance commissioner — the process is free and designed for consumers to use without legal help. However, if your dispute involves bad faith conduct or a large settlement gap exceeding $10,000, consulting an insurance attorney before or alongside your complaint is advisable. An attorney can advise you on whether your situation justifies litigation and ensure your complaint does not inadvertently harm a future legal claim.

Can my insurance company cancel my policy if I dispute the settlement?

An insurer cannot legally cancel your policy solely because you disputed a settlement — doing so would constitute retaliation and violate state insurance codes in every U.S. jurisdiction. However, filing multiple claims over a short period can affect your renewal eligibility as a separate matter. Your right to dispute an insurance settlement is explicitly protected under consumer protection statutes and insurance regulations at both the state and federal level.

Does filing a claim dispute affect my insurance rates?

Disputing a settlement amount — as opposed to filing a new claim — does not by itself trigger a rate increase. Rate increases are triggered by new claims, not by disputes over existing claim valuations. That said, if your dispute results in the insurer paying significantly more than initially offered, some insurers may flag the claim for underwriting review at renewal. Review how deductibles and premiums interact to understand the full cost picture of your claim strategy.

What is the appraisal clause and does every insurance policy have one?

The appraisal clause is a policy provision that allows both the insurer and the policyholder to demand an independent assessment of the loss amount when they cannot agree. Most standard homeowners policies issued under ISO HO-3 or HO-5 forms include an appraisal clause, and many auto policies do as well. It is a binding, non-litigation resolution mechanism that bypasses the court system entirely — making it one of the fastest and most cost-effective ways to resolve a dispute insurance settlement standoff.

How do I write a demand letter to dispute an insurance settlement?

A demand letter to dispute an insurance settlement should be concise, specific, and evidence-driven. Open with your claim and policy number, state clearly that you are disputing the offer, specify the exact dollar amount you are demanding, and list each piece of supporting evidence you are enclosing. Send it via certified mail with return receipt. Close with a reasonable response deadline — 14 to 21 days — and a statement that you will escalate to your state insurance department if a satisfactory response is not received.

Sources

- Insurance Information Institute — Homeowners and Renters Insurance Facts and Statistics

- National Association of Insurance Commissioners (NAIC) — Insurance Claims Consumer Resources

- National Association of Public Insurance Adjusters (NAPIA) — Consumer Information

- NAIC Consumer Information Source — State Insurance Department Directory

- California Department of Insurance — Consumer Complaint Center

- NAIC — Insurance Department Complaint Data White Paper

- NAPIA — Find a Licensed Public Adjuster Directory

- United Policyholders — Fighting Your Insurance Company Guide

- Florida Department of Financial Services — Insurance Mediation Program

- Federal Trade Commission — Insurance Consumer Protection Resources