Fact-checked by the The Insurance Scout editorial team

Quick Answer

Standard homeowners insurance typically caps business property coverage at just $2,500 and provides zero liability protection for business-related injuries or losses at your home. As of July 2025, home-based business owners need to add an in-home business endorsement, a BOP, or a standalone commercial policy to close these dangerous coverage gaps.

If you run a business from home and rely solely on your homeowners policy for protection, you are likely one client visit or equipment theft away from a denied claim. Home business homeowners insurance gaps affect millions of Americans — the U.S. Small Business Administration estimates that more than 50% of all small businesses are home-based — yet standard homeowners policies were never designed to cover commercial activity. As of July 2025, this mismatch is one of the most common and costly coverage blind spots in personal insurance.

The insurance industry has accelerated product development for home-based workers in recent years, driven by the remote-work boom that permanently expanded home office culture after 2020. Insurers including State Farm, Allstate, and Erie Insurance now offer dedicated endorsements, but most policyholders never think to ask. The result: billions in uninsured business losses each year that homeowners assume their existing policy covers.

This guide is for freelancers, consultants, e-commerce sellers, tutors, childcare providers, and any professional running a business from a residential address. By the end, you will know exactly what your current policy covers, where it falls short, and how to build a complete coverage plan without overpaying.

Key Takeaways

- Most standard homeowners policies limit business personal property coverage to $2,500 on-premises and only $500 off-premises, according to the Insurance Information Institute.

- A home-based business endorsement typically costs between $25 and $75 per year, making it one of the cheapest coverage upgrades available, per III data.

- A Business Owner’s Policy (BOP) bundles general liability and commercial property coverage and is available to qualifying home-based businesses for as little as $500 per year.

- Homeowners policies explicitly exclude liability for business activities, meaning a client injured at your home office could sue you personally with no insurer backing you, as noted by the Insurance Information Institute.

- Professional liability (errors and omissions) insurance is separate from general liability and is critical for service-based businesses — average premiums run $500 to $1,000 per year for solo operators.

- Freelancers and self-employed workers who already manage complex coverage needs can find broader context in our guide to building a solid insurance safety net as a freelancer or gig worker.

In This Guide

- Step 1: What Does My Homeowners Policy Actually Cover for My Home Business?

- Step 2: How Do I Identify the Specific Coverage Gaps for My Type of Business?

- Step 3: Should I Add a Home Business Endorsement or Get a Separate Business Policy?

- Step 4: What Types of Business Insurance Coverage Do I Actually Need?

- Step 5: How Do I Add Home Business Coverage to My Existing Homeowners Policy?

- Step 6: How Do I Avoid Having a Home Business Claim Denied?

- Frequently Asked Questions

Step 1: What Does My Homeowners Policy Actually Cover for My Home Business?

Your standard homeowners policy covers your home business equipment and liability only in the most limited way — and often not at all for commercial activity. Understanding these limits is the essential starting point before shopping for supplemental coverage.

What the Standard Policy Actually Says

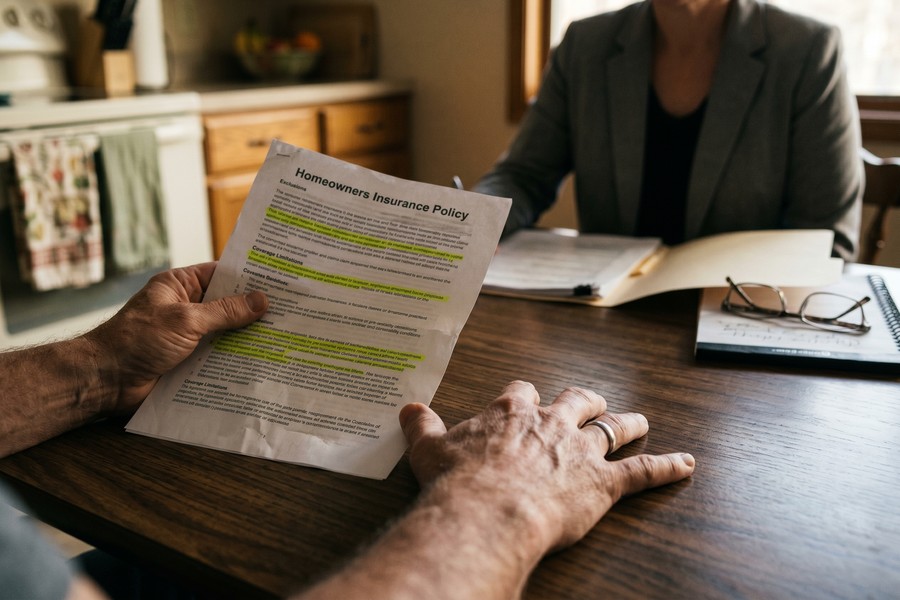

A standard HO-3 homeowners policy — the most common form in the U.S. — includes two specific business-related restrictions. First, it limits business personal property (computers, cameras, inventory, tools) to $2,500 on your premises and just $500 if the equipment is away from home. Second, it explicitly excludes liability arising from any business pursuits conducted at the property.

That liability exclusion is the more dangerous gap. If a client trips and falls in your home office, your homeowners liability coverage will almost certainly deny the claim. The insurer will argue the injury arose from a business activity, not a residential one.

What “Business Pursuits” Means to an Insurer

Insurers define business pursuits broadly. Selling products on Etsy, giving piano lessons, running a daycare, providing bookkeeping services — all of these qualify. Even a single paid transaction can trigger the exclusion in a claim dispute. Many policyholders are surprised to learn this after a loss, not before.

It is also worth reviewing common policy mistakes that lead to denied claims. Our breakdown of homeowners insurance mistakes that lead to denied claims covers several scenarios directly relevant to home business owners.

Never assume that because your laptop is used for both personal and business tasks, it is fully covered. Insurers look at primary use. If your primary use is business, the $2,500 cap — not your full coverage limit — applies, and depreciation may reduce that further.

Step 2: How Do I Identify the Specific Coverage Gaps for My Type of Business?

Your coverage gaps depend entirely on your business type, how many clients visit your home, the value of your equipment, and whether you carry inventory. A graphic designer has different exposures than a daycare operator or an online retailer with $20,000 in stored goods.

Map Your Business Exposures

Work through these four exposure categories to identify where you are unprotected:

- Business property: Add up the replacement value of all business equipment, inventory, and supplies. If that total exceeds $2,500, you have a gap.

- Liability — bodily injury: Do clients, delivery drivers, or employees visit your home? Each visit creates potential liability your homeowners policy will not cover.

- Liability — professional errors: Do you give advice, design things, or provide a service that could harm a client financially? General liability does not cover professional errors — you need a separate errors and omissions (E&O) policy.

- Business income: If a covered event (fire, windstorm) forced you to stop working, would your homeowners policy replace lost revenue? No — standard policies have no business income protection.

What to Watch Out For

Home daycare and childcare businesses face the strictest insurer scrutiny. Many insurers will non-renew or cancel a homeowners policy entirely if they discover unlicensed childcare is being conducted on the premises. Check your state’s licensing requirements and disclose your business use to your insurer in writing.

According to the Insurance Information Institute, roughly 60% of home-based business owners have no additional business insurance beyond their standard homeowners or renters policy — leaving the majority underinsured.

Step 3: Should I Add a Home Business Endorsement or Get a Separate Business Policy?

For most home-based businesses with fewer than five employees and under $250,000 in annual revenue, the choice comes down to three options: a home business endorsement, an in-home business policy, or a standalone Business Owner’s Policy (BOP). Each suits a different scale and risk profile.

The Three Coverage Options Compared

A home business endorsement (also called a rider) is the simplest fix. You add it to your existing homeowners policy, typically for $25 to $75 per year. It raises your business property limit to roughly $10,000 and adds limited liability coverage. It is best for very low-risk businesses with minimal equipment and no client visits.

An in-home business policy is a step up — a separate but related policy issued by your home insurer. It typically offers up to $100,000 in business property and $300,000 in liability coverage. Annual premiums generally run $150 to $400.

A standalone BOP is the most comprehensive option and the right choice for businesses that carry significant inventory, have employees, or regularly host clients. A BOP bundles commercial property insurance, general liability, and often business interruption insurance into one policy.

| Coverage Option | Business Property Limit | Liability Limit | Business Income | Typical Annual Cost | Best For |

|---|---|---|---|---|---|

| Standard HO-3 (No Add-On) | $2,500 on-premises / $500 off | $0 for business activity | Not included | $0 extra | Nobody running a real business |

| Home Business Endorsement | Up to $10,000 | $300,000 | Not included | $25–$75/year | Writers, consultants, very low risk |

| In-Home Business Policy | Up to $100,000 | $300,000 | Sometimes included | $150–$400/year | Solo professionals, tutors, artists |

| Business Owner’s Policy (BOP) | Up to $1,000,000+ | $1,000,000+ | Included | $500–$3,000/year | Retailers, contractors, childcare, employees |

| Professional Liability / E&O | Not covered | $1,000,000 (claims-made) | Not included | $500–$1,500/year | Consultants, designers, accountants |

“Most home-based business owners do not realize that a single client injury on their property — or even an allegation of professional negligence — can wipe out personal savings in legal fees alone. The gap between what a homeowners policy provides and what a business actually needs is enormous, and it closes for less money than most people think.”

What to Watch Out For

Some insurers will not offer an endorsement if your business generates more than $5,000 per year in revenue. Always disclose your actual annual revenue when applying — misrepresentation is grounds for claim denial and policy cancellation. If your revenue exceeds that threshold, go directly to a BOP or standalone commercial policy.

Ask your current homeowners insurer first. Many carriers — including Nationwide, State Farm, and Allstate — offer in-house business endorsements that keep all your policies under one roof, simplifying claims coordination and often qualifying you for a multi-policy discount.

Step 4: What Types of Business Insurance Coverage Do I Actually Need?

The right coverage stack for a home-based business typically combines four building blocks: commercial property, general liability, professional liability, and business income protection. Not every business needs all four, but most need at least the first two.

Commercial Property Insurance

Commercial property insurance covers physical business assets — computers, printers, inventory, furniture, and specialized equipment — at their full replacement cost rather than the depreciated actual cash value most homeowners policies default to. If you are unsure which valuation method your current policy uses, our comparison of actual cash value vs. replacement cost coverage explains exactly what the difference costs you at claim time.

For e-commerce sellers and product-based businesses, inventory coverage is especially critical. A fire or burst pipe that destroys $15,000 in merchandise will not be covered by a homeowners policy — and may not even be covered by a basic endorsement, depending on the insurer’s product inventory sublimits.

General Liability Insurance

General liability (GL) insurance covers bodily injury, property damage, and advertising injury claims made by third parties. A client who slips on your icy driveway while visiting your home office can file a claim under your GL policy. GL limits for home-based businesses typically start at $300,000 and go up to $2 million per occurrence.

Professional Liability (Errors and Omissions)

Professional liability insurance — also called errors and omissions (E&O) — covers claims that your advice, design, or service caused a client financial harm. It is separate from general liability and is essential for consultants, graphic designers, financial advisors, accountants, tutors, and any other service-based business. A dissatisfied client can sue for the cost of redoing your work, lost contracts, or other financial damages — none of which general liability covers.

Business Income (Business Interruption) Insurance

Business income insurance replaces lost revenue and covers ongoing fixed expenses if a covered disaster forces you to stop operating. For a home-based business, this is often bundled into a BOP. Without it, a single event like a kitchen fire could cost you months of income while your home is repaired.

Workers’ compensation insurance may be legally required even for a home-based business with just one part-time employee. Requirements vary by state — the U.S. Department of Labor’s Wage and Hour Division maintains state-by-state guidance on employer obligations.

Step 5: How Do I Add Home Business Coverage to My Existing Homeowners Policy?

Adding home business coverage is a straightforward three-step process: disclose your business to your current insurer, request a quote for an endorsement or standalone policy, and compare options before binding. Most people complete this in under a week.

How to Do This

Start by calling your current homeowners insurer and clearly disclosing the nature of your business, your annual revenue, whether clients visit your home, the number of employees, and the estimated replacement value of all business property. This disclosure protects you — failure to inform your insurer of material changes in how you use your home is one of the most common reasons claims are denied, as detailed in our article on homeowners insurance mistakes that lead to denied claims.

Next, request quotes from at least three sources: your current carrier, an independent insurance agent who can access multiple commercial markets, and a direct commercial insurer like Hiscox, Next Insurance, or Thimble, which specialize in small and micro-business coverage with online quoting in minutes.

When comparing quotes, look beyond the premium. Compare the per-occurrence liability limit, the business property limit, whether inventory is covered, and whether professional liability is included or must be added separately.

What to Watch Out For

Some carriers will respond to your disclosure by non-renewing your homeowners policy if they consider your business activity too high-risk for their residential book. This is more common with daycare, food production, and businesses involving hazardous materials. If this happens, work with an independent agent who can find a carrier willing to write both your home and business coverage.

If your business has grown significantly, it may also be time to reassess other parts of your personal coverage. Major business growth is a life event that can affect multiple policies — our guide on what to update after a major life event walks through the full checklist.

Thimble and Next Insurance both offer monthly pay-as-you-go BOP options with coverage that can start the same day. For seasonal businesses or new ventures not yet generating consistent revenue, monthly billing eliminates the upfront cost of an annual premium.

Step 6: How Do I Avoid Having a Home Business Claim Denied?

The most common reason home business insurance claims are denied is that the policyholder failed to disclose business activity at the time of application or renewal. Preventing denial comes down to documentation, disclosure, and keeping your coverage updated as your business grows.

How to Do This

Keep a detailed, updated inventory of all business equipment with serial numbers, purchase prices, and receipts. Store this inventory file in cloud storage (not just on a local drive that could be destroyed in the same event you are claiming). Insurers require proof of ownership and value for business property claims, and gaps in documentation consistently reduce or void payouts.

Review your policy at every renewal — typically annually. If your business revenue, headcount, equipment value, or client visit frequency has changed, notify your insurer in writing before renewal. A formal written notification creates a paper trail that protects you if a claim is disputed.

If you make physical changes to your home to support your business — converting a garage into a studio, building a separate entrance for clients — notify your homeowners insurer immediately. Structural changes affect your dwelling coverage and can void your policy if undisclosed. Our guide to how home renovations affect your homeowners insurance covers this in detail.

What to Watch Out For

Never file a claim under your homeowners policy for a loss you know was business-related. If the insurer investigates — which they often do for larger claims — and finds evidence of business activity, they can deny the claim entirely and potentially cancel your policy for misrepresentation. Always route business losses through your business policy.

“Documentation is everything in a business property claim. We see cases where a home-based business owner has $30,000 in equipment but can only substantiate $8,000 because they never kept records. The payout reflects what you can prove, not what you say you had.”

If your home-based business involves employees — even part-time or 1099 contractors who work on-site — your liability exposure increases dramatically. A general liability policy alone is not sufficient. Consult an independent commercial insurance agent about employer liability and workers’ compensation requirements in your state.

Frequently Asked Questions

Does my homeowners insurance cover my home office equipment?

Your standard homeowners policy covers business equipment only up to $2,500 on your premises — not the full replacement value. If your laptop, camera, printer, or other business tools exceed that combined value (which most do), you need a home business endorsement or commercial property policy to cover the difference. Off-premises coverage drops to just $500 under most standard policies.

What happens if a client gets injured at my home office?

Your standard homeowners liability coverage will likely deny the claim because the injury arose from a business activity, which is explicitly excluded from most HO-3 policies. Without a separate business liability policy or endorsement, you would be personally responsible for medical bills, legal fees, and any settlement. General liability coverage for home-based businesses starts at around $300,000 and typically costs less than $400 per year.

Can I get home business homeowners insurance if I sell products online?

Yes, but a basic homeowners endorsement is almost certainly not enough for an e-commerce seller. You need commercial property coverage for your inventory, product liability coverage in case a product you sell injures a buyer, and potentially business income coverage. A BOP is typically the most cost-effective solution, with policies available from carriers like Next Insurance and Hiscox starting around $500 per year for low-volume sellers.

Will my homeowners insurance go up if I tell them I run a business from home?

Simply disclosing business use may result in a modest premium increase, but the more likely outcome is that your insurer will require you to add an endorsement or refer you to a commercial policy. Hiding business activity to avoid a rate increase is far riskier — it can result in full claim denial and policy cancellation when discovered. The premium difference for an endorsement is typically under $75 per year.

Do I need professional liability insurance for my home-based consulting business?

Yes, if you provide advice, analysis, or specialized services for a fee. General liability covers physical injury and property damage, but it does not cover claims that your professional advice caused a client financial harm. Errors and omissions (E&O) insurance covers those claims, and for solo consultants it typically costs between $500 and $1,000 per year. Most BOPs do not include E&O — it must be added separately.

What is the difference between a home business endorsement and a BOP?

A home business endorsement is a rider added to your existing homeowners policy, typically raising business property coverage to $10,000 and adding limited liability — best for very low-risk, low-revenue businesses. A Business Owner’s Policy (BOP) is a standalone commercial policy that combines commercial property, general liability, and business income insurance — better for businesses with employees, regular client visits, significant inventory, or higher revenue. A BOP costs more but offers far broader protection.

Is my business vehicle covered under my homeowners policy?

No. Business use of a vehicle — including transporting products, equipment, or clients — is excluded from both homeowners and standard personal auto policies. If you use your car primarily for business purposes, you need a commercial auto policy or a business-use endorsement on your personal auto policy. Rideshare-style coverage gaps follow a similar logic, as explored in our guide to what Uber and Lyft auto insurance doesn’t cover.

Can my homeowners insurance be cancelled because I run a business from home?

Yes, in some cases. High-risk business types — including unlicensed daycare, food production, firearms sales, or businesses with frequent client traffic — can prompt a carrier to non-renew your homeowners policy at renewal. Proactive disclosure gives you time to find a carrier that writes both residential and commercial coverage. Waiting until a claim is filed to disclose business activity is far worse — it can result in retroactive cancellation.

How much does home-based business insurance cost per month?

Costs vary widely by business type, revenue, and coverage level. A basic home business endorsement runs $2 to $6 per month. An in-home business policy averages $12 to $33 per month. A full BOP for a solo home-based business typically costs $42 to $250 per month, depending on industry risk, revenue, and location. Professional liability adds another $40 to $125 per month for most solo service providers.

Do I need home business insurance if I only work from home part time?

Part-time status does not reduce your liability exposure — a client can be injured during a single visit, and one professional error can generate a lawsuit regardless of how many hours per week you work. The homeowners policy business exclusion applies whether you operate full-time or just a few hours a week. Even a $25-per-year endorsement is worth adding the moment you conduct any paid business activity from your home address.

Sources

- Insurance Information Institute — Home-Based Business Insurance

- U.S. Small Business Administration — Home-Based Businesses

- U.S. Department of Labor — Wage and Hour Division

- United Policyholders — Insurance Resources for Homeowners

- National Association of Insurance Commissioners — Home-Based Business Consumer Alert

- Insurance Information Institute — Business Owner’s Policy (BOP)

- Insurance Information Institute — What Is Covered by a Standard Homeowners Policy

- Investopedia — Homeowners Insurance Overview

- Hiscox — Home-Based Business Insurance

- U.S. Census Bureau — Working From Home During the Pandemic